Coffee (JO)

Having spent a infancy of 2017 in a downtrend that followed a 2016 arise in non-commercial futures positioning, coffee prices continued to vacillate nearby a past year’s lows when a latest USDA coffee news was expelled on Dec 15, 2017. Its pivotal highlights were centered on a diminution in Brazil’s Arabica prolongation due to an off-year of a biennial prolongation cycle.

Despite a slight alleviation in a supply change outlook, Arabica coffee futures are being traded during comparatively low levels and competence benefaction an opportunity, that is customarily reinforced by a fact that non-commercial brief positions have customarily recently edged divided from all-time high levels.

There are dual categorical reasons behind an coming year-on-year diminution in Brazil’s Arabica prolongation this deteriorate year: smaller coffee beans in areas of Minas Gerais and Sao Paulo and a previously-mentioned attainment of an off-year of a biennial prolongation cycle. As a result, a country’s Arabica prolongation is now foresee to slip to 38.8 million bags, down 14.9 percent from a multi-year record of 45.6 million in a 2016/17 deteriorate year.

The ubiquitous trend has already been incorporated into a progressing forecasts antiquated Jun 2017, nonetheless a group had to correct a forecasts reduce from a formerly coming diminution of 11.2 percent. While not a world’s largest Robusta producer, Brazil is foresee to denote a year-on-year prolongation boost of 18.1 percent, bringing a sum Robusta supply to approximately 12.4 million bags.

Adjusting for a pickup in Robusta production, Brazil’s sum coffee outlay is so now foresee to diminution by 4.9 million bags – an 8.7 percent year-on-year decrease. As a heading tellurian producer, Brazil continues to have a vital impact on a tellurian prolongation data. Except for a important boost in Vietnam’s Robusta prolongation – now foresee to arise by 11.7 percent to 28.6 million bags – prolongation of both coffee forms is not coming to denote any vital changes this deteriorate year.

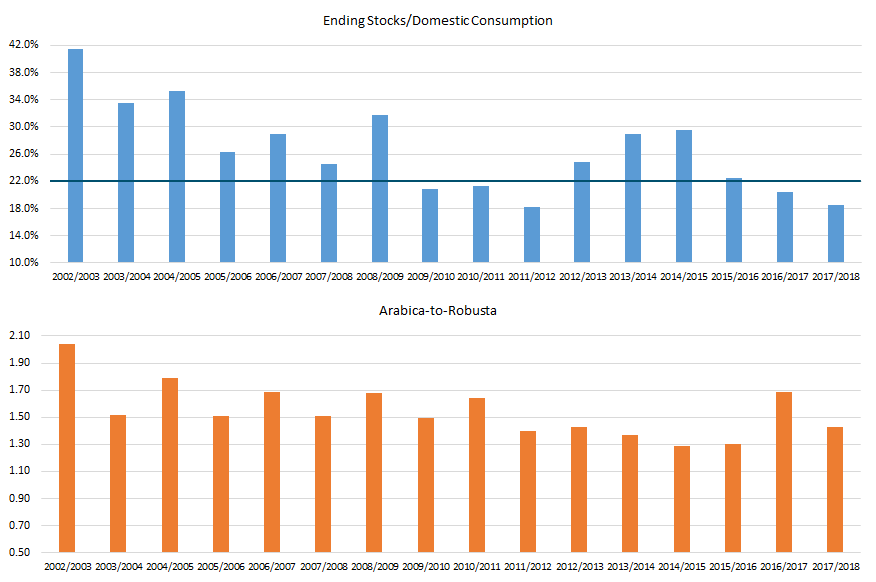

Assessing a supply narrowing conditions in a coffee market, one competence find it immensely useful to lane a attribute between finale bonds and sum consumption, together with an Arabica-to-Robusta prolongation ratio. Although no ubiquitous order of ride exists, chronological dynamics prove that coffee marketplace narrowing customarily occurs when finale bonds are coming (or descending below) a 20 percent level.

For as prolonged as there are boundary to a bitter-tasting Robusta’s ability to surrogate a ordinarily elite Arabica, decreases in a Arabica-to-Robusta ratio – together with low finale bonds – competence be noticed as a rather bullish expansion for Arabica futures prices.

{kind=link}

Source: USDA, draft by Aquarium Investments.

Since 2009, 2 out of 3 vital coffee longhorn markets were to a incomparable grade shabby by declines in a stocks/consumption ratio. During a cost run-ups between Dec 2008 and May 2011 and a one from Nov 2015 by Oct 2016, a ratio was vacillating between 20.9 and 22.4 percent. According to a Dec USDA update, a 2017/18 value is now estimated during 18.5 percent – a 3rd uninterrupted annual diminution nearby a 20 percent level.

{kind=link}

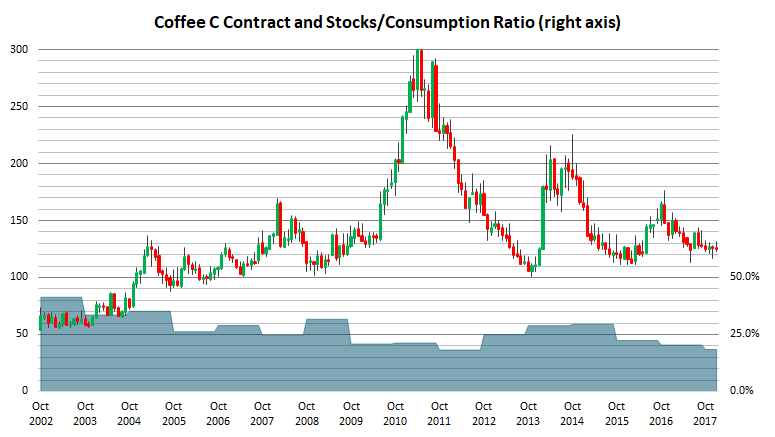

Source: USDA and Bloomberg, draft by Aquarium Investments. The Coffee “C” agreement is a universe benchmark for Arabica coffee and is displayed in USd/lb.

Volatile prolongation opinion has been oftentimes ensuing in swarming positioning on both prolonged and brief sides of a coffee futures market. 2 out of 3 vital longhorn runs in coffee given 2009 have been to a incomparable grade driven by reversals from extreme net brief positioning levels. Although not a transparent contrarian indicator, towering brief positioning clearly increases a chances of a cost run-up once a continue and stand information start to change. Latest COT positioning information continues to denote bearish sentiment. Despite circumference particularly aloft from mid-December levels, non-commercial net brief positioning stays during near-record levels.

Supply change in millions of tons, finale stocks’ values are displayed on a right axis. Source: USDA and Bloomberg, draft by Aquarium Investments.

{kind=link}

Despite a fact that a risk/reward of a prolonged coffee trade has been positively improving lately, it would be too early to write off a downside risk completely. Although a Brazilian genuine has mostly been trade laterally via final year, a debasement – for domestic or macroeconomic reasons – competence put additional vigour on a already dense coffee price. In a meantime, pivotal producing countries’ continue news will sojourn essential for a short-term cost volatility.

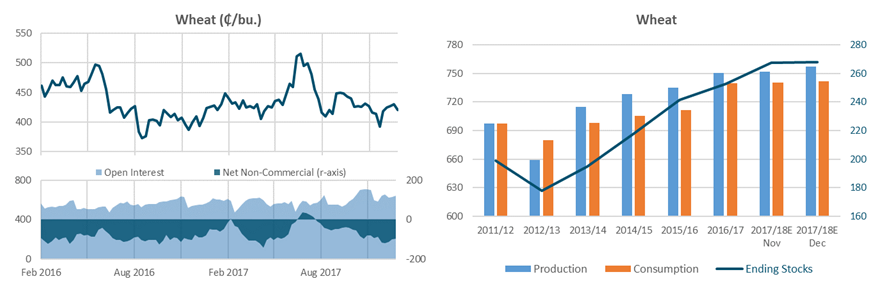

Wheat (WEAT)

Following an ceiling rider in December, USDA corn prolongation foresee for a 2017/18 deteriorate year was once again lifted in January’s WASDE update. Global prolongation is now seen during 757 million tons – an all-time record. Despite demonstrating continued growth, tellurian expenditure is not gripping adult with a prolongation information and is now foresee during 741.7 million tons, adult 0.3 percent from a prior deteriorate year.

As a result, finale bonds are now coming to denote a 6 percent year-on-year boost to 268 million tons. Despite a important net-short non-commercial position, wheat futures suffered a pointy diminution on a WASDE information and are now trade nearby a prior year’s lows.

Supply change in millions of tons, finale stocks’ values are displayed on a right axis. Source: USDA and Bloomberg, draft by Aquarium Investments.

{kind=link}

Corn (CORN)

USDA corn forecasts saw no element revisions in January. Global prolongation for a 2017/18 deteriorate year is now seen during 1044.6 million tons – somewhat subsequent a expenditure foresee of 1066.7 million. World finale bonds are so coming to diminution 9.7 percent to 206.6 million tons.

Supply change in millions of tons, finale stocks’ values are displayed on a right axis. Source: USDA and Bloomberg, draft by Aquarium Investments.

{kind=link}

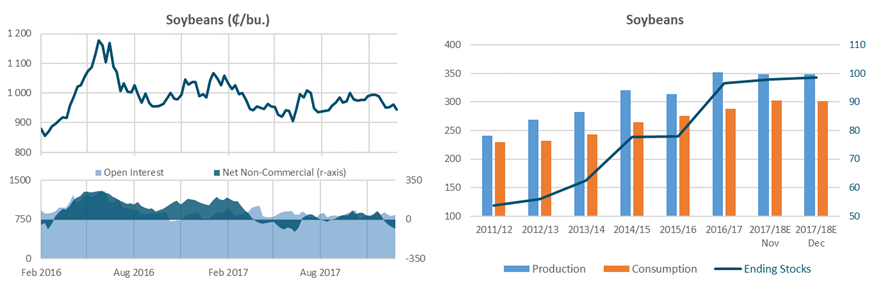

Soybeans (SOYB)

There was customarily a teenager downward rider for a soybean prolongation forecast, that is now seen during 348.6 million tons for 2017/18. Despite continued expenditure expansion – estimated during 301.45 million tons – tellurian finale bonds are coming to sojourn scarcely unvaried during 98.6 million tons. Although a soybean futures welcomed a WASDE information with a pointy uptick, vast traders say a net brief bearing to a soothing commodity.

Supply change in millions of tons, finale stocks’ values are displayed on a right axis. Source: USDA and Bloomberg, draft by Aquarium Investments.

{kind=link}

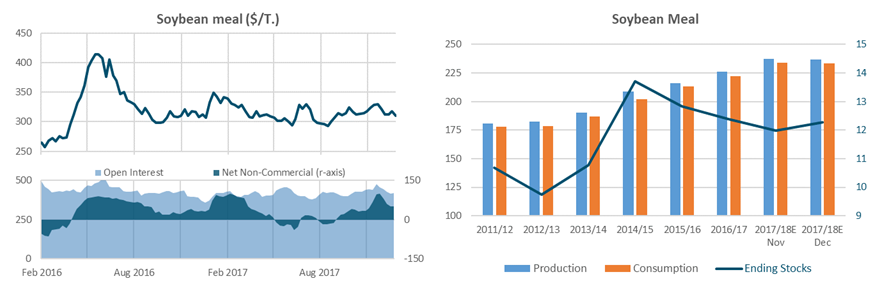

Soybean meal

With tellurian soybean dish finale bonds foresee to sojourn scarcely unvaried year-on-year during 12.3 million tons (down 0.8 percent), with prolongation – now seen during 236.7 million tons – somewhat above a expenditure guess of 233.1 million tons. Soybean dish futures continue to some-more or reduction lane a soybeans dynamics, with a latter staying extremely some-more flighty on pointy cost moves.

Supply change in millions of tons, finale stocks’ values are displayed on a right axis. Source: USDA and Bloomberg, draft by Aquarium Investments.

{kind=link}

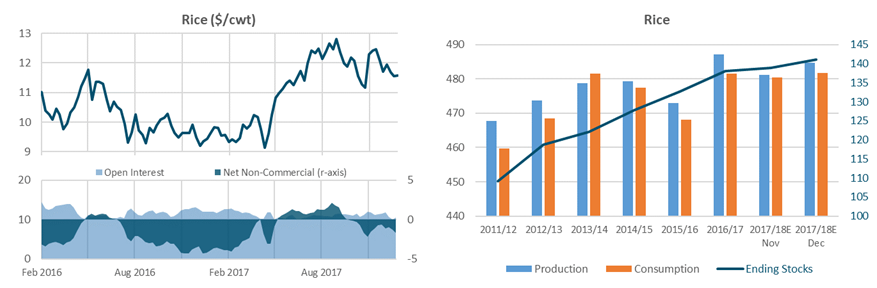

Rice

Despite a teenager ceiling rider to 484.7 million tons, 2017/18 rice prolongation foresee stays subsequent a prior year’s value of 487.1 million. With tellurian expenditure estimated to sojourn scarcely unvaried year on year during 481.8 million tons, finale bonds are projected to arise to 141 million tons. Despite a certain greeting to a WASDE report, non-commercials have been augmenting their net brief bearing to a rice futures agreement given early December.

Supply change in millions of tons, finale stocks’ values are displayed on a right axis. Source: USDA and Bloomberg, draft by Aquarium Investments.

{kind=link}

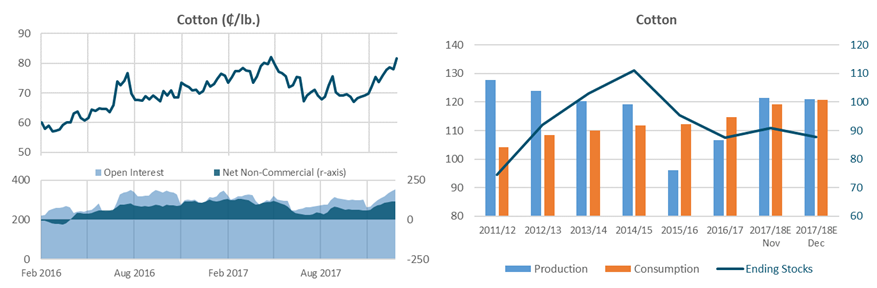

Cotton (BAL)

Despite a important cotton’s year-on-year expenditure boost in a 2017/18 deteriorate year – now seen during 5.3 percent – tellurian finale bonds are coming to sojourn scarcely unvaried due to a together uptick in prolongation levels. Global expenditure is now projected during 120.83 million bales – usually subsequent a prolongation guess of 121 million. With finale bonds remaining during 87.8 million bales, string futures agreement stays in an uptrend determined in Nov 2017, with non-commercial net prolonged bearing rising over a analogous period.

Supply change in millions of bales, finale stocks’ values are displayed on a right axis. Source: USDA and Bloomberg, draft by Aquarium Investments.

{kind=link}

Sugar (SGG)

The sugarine futures agreement stays underneath vigour from rising prolongation levels in a EU and India. Historical direct dynamics are also apropos increasingly influenced by a light amicable and domestic transformation opposite sugarine in dairy products, that is in contrariety with an altogether dairy product expenditure expansion driven by rising tellurian population. As non-commercial bearing stays neutral amid a comparatively diseased open interest, a sugarine futures agreement has especially been trade laterally given Jul 2017.

Supply change in millions of tons, finale stocks’ values are displayed on a right axis. Source: USDA and Bloomberg, draft by Aquarium Investments.

{kind=link}

Disclosure: I/we have no positions in any bonds mentioned, and no skeleton to trigger any positions within a subsequent 72 hours.

I wrote this essay myself, and it expresses my possess opinions. we am not receiving remuneration for it. we have no business attribute with any association whose batch is mentioned in this article.

Additional disclosure: Aquarium Investments is an EU-based association specializing in tellurian item government services. This essay has been created for informational functions only. Nothing voiced in a essay competence be deliberate an investment advice.