2019’s rush of IPOs isn’t vouchsafing up. While Lyft (LYFT) and Uber (UBER) have grabbed a many headlines, there’s copiousness of other fad around. A lot of good companies have left open this year. Some of a IPOs, like Beyond Meat (BYND), finished clarity during their IPO cost nonetheless are resembling a dot-com insanity some-more and some-more nowadays.

While it’s too early to announce if Luckin Coffee (LK) will join a large winners like Beyond or be another broken like Lyft has been so far, we can make a guesses. And while anything can happen, it will take things going usually right for Luckin’s business indication to be a suggestive success. Unfortunately, a closest new IPO analogue we can come adult with for Luckin would be Nio (NIO).

Nio, for those unfamiliar, represented itself as a intensity Tesla (TSLA) killer. Whether we need a Tesla-killer given Tesla’s terrible happening recently is debatable. In any case, it’s looking like Nio isn’t going to be a one a throws punches during Musk Co. Since a hyped adult 60 Minutes appearance progressing this year, NIO batch has collapsed in value:

Data by YCharts

Data by YChartsWhy has Nio collapsed? Because it’s blazing income during an pornographic rate while offered comparatively few cars. Change a word “cars” for “coffee” and that prior judgment describes Luckin as well. Like Nio, Luckin is spooky with flourishing as quick as probable with minimal regard for costs. Also, like Nio, it’s vigilant on portraying itself as a tech association nonetheless a genuine business – sell – is decidedly some-more prosaic.

Luckin: Not The Starbucks Of China

Investors like to report companies as a “X” of “Y” to assistance people know a business. These analogies can be dubious though. Unless a companies are scarcely CO copies, a lot can get mislaid when we fit a unfamiliar organisation into a informed mental indication of a domestic counterpart.

In a box of Luckin, they won’t be a Starbucks (SBUX) of China unless they radically renovate their business model. That’s because, we find in their prospectus, 91% of their stream stores are set adult for take out and have minimal seating capacity.

So many of what has finished Starbucks successful is being a supposed third place. Somewhere that wasn’t your home or your bureau where we could hang out with friends, review a book, get some computing work done, or whatever. we remember people suggesting behind around a Dunkin Donuts (DNKN) IPO years ago that it could turn a critical aspirant to Starbucks as it stretched with all a IPO proceeds. But that sight of suspicion missed a point. Dunkin isn’t competing with Starbucks. People don’t go to Dunkin to hang out for hours. Dunkin’s foe is closer to a McCafe’s or preference stores of a universe that also sell prohibited brewed coffee.

Similarly, as prolonged as Luckin usually has a tiny apportionment of a store bottom oriented toward lay down, hang out locations, it isn’t targeting a same niche as Starbucks directly. Sure there’s overlie – both are creation large pushes for smoothness business where foe is some-more approach for instance – nonetheless it’s not a core conflict front between a dual brands.

As China business consultant Jeffrey Towson noted, Luckin is environment adult in cheaper off-main travel locations, given Starbucks tends to secure a best, highest-trafficked many costly locations available. Not surprisingly, as Luckin is competing heavily on cost, it needs to keep over down. Forgoing a pivotal principle of Starbucks’ strategy, good locations, helps with that.

Huge Losses

Now that we have that pivotal bit about a business indication out of a way, we can start digging into a numbers. Luckin impossibly grew from usually a handful of stores during a finish of 2017 to several thousand by a finish of 2018. It intends, according to a prospectus, to pass Starbucks and have a many stores of any Chinese coffee sequence by a finish of this year.

Not surprisingly, this arrange of raging enlargement leads to extreme waste as well. New sell concepts generally don’t turn evident income spinners. It takes time to build code faithfulness and awareness.

However, Luckin’s loss-making goes over anything we can remember saying in sell before. The devise is audacious, to contend a least. In a latest quarter, they managed to remove $78 million while offered usually $71 million of product. That’s an handling domain of over -100%, amazingly enough.

The sum domain stinks here too. The company’s cost of materials sole was $41 million on those $71 million of sales. we don’t even know how this is probable when your submit costs (coffee beans, water, sugar, cups) are so cheap. Starbucks is scandalous for a enormous distinction margins. Needless to say, McDonald’s (NYSE:MCD) can do glorious offered coffee during 99 cents or whatever low cost it’s during today. You don’t need to assign $4 to make a distinction in this business.

So Luckin, with prices something like modestly subsequent Starbucks, should be during slightest creation a decent sum margin. Yes, we know they are discounting like crazy to attract customers. But still, this is coffee we’re articulate about, not a high-cost food like smoked salmon or something.

Store let and other handling waste gets we another $42 million in costs final quarter. So we’re already adult to $93 million of waste to beget $71 million in sales. And that’s before we strike any other costs such as SGA or marketing. At Luckin’s stream scale, this business indication is officious dreadful.

Keep in mind that simply adding some-more stores doesn’t do all that many for we either. Costs such as labor and lease enhance sincerely linearly with any new store. Yes, we save some on selling and corporate over as we supplement some-more stores. But when you’re already losing a supernatural volume of income on any sale usually accounting for a cost of products sole and store rent, building new stores isn’t indispensably going to grow your approach out of a mess. Simply put, Luckin needs some-more sales – distant some-more – per existent store to have any possibility of ever reaching profitability. And as we’ll see in a minute, there are signs that Luckin’s ceiling sales arena has already slowed dramatically.

Can The Business Model Work?

Reading a prospectus, when we come to a devise section, underneath business strengths, dual of a initial 3 they list engage tech. These are “pioneer of disruptive new business model” and “strong technological capabilities.” In essence, Luckin wants to be deliberate a tech association in a same approach that Jim Cramer labeled Domino’s (DPZ) a tech association given of a nifty app.

But let’s delayed down a minute, any grill or tradesman can offer people a new or softened app. That doesn’t make them all tech companies. Once a tech glitz fades, you’ve still got a sell coffee business here with widely homely economics (at slightest for a time being). There’s some-more wrong than usually a outrageous handling loss.

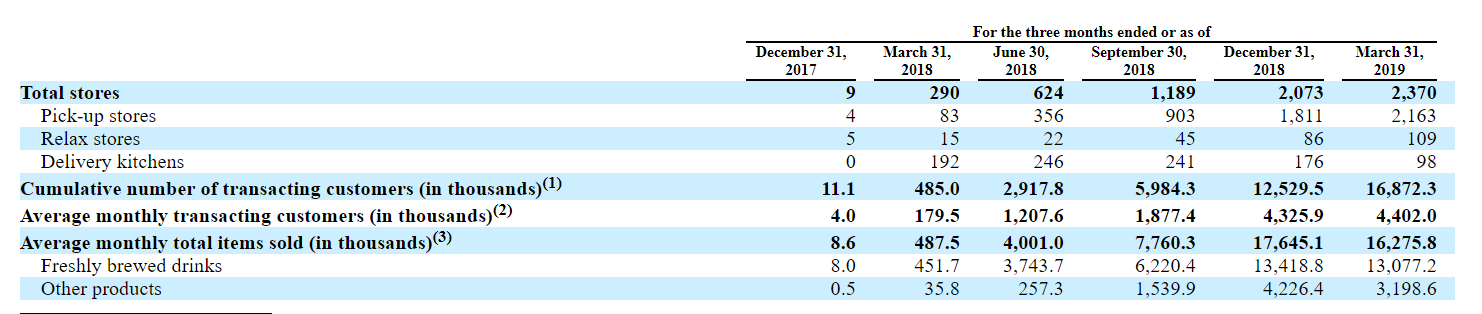

We see in a handbill an shocking enlargement in a latest quarter:

Did we locate it? Despite a association opening a net 297 new stores, normal monthly transacting business was radically flat, and normal monthly sum equipment sole indeed forsaken by roughly 10%. There could be some uncanny gift that explains this. For instance maybe a smoothness kitchens they have been shutting beget some-more normal sales than a pick-up stores.

Without some-more clarity on this though, a initial takeaway is awful. If we open 297 new stores – a scarcely 15% enlargement on a store bottom – we should see a vital uptick in both sum business and sales volume. What’s going on here? Also, interestingly, this was their slowest entertain opening stores given Mar of final year. In Q4, they non-stop some-more than 800 net stores. Why a remarkable dump in new store activity now?

A asocial chairman competence theory that a new stores aren’t operative as designed – and as a sales information is starting to uncover – and hence because we got a IPO during this accurate impulse in time. Needless to say, if Luckin’s ability to grow a Chinese coffee marketplace already is petering out now, with a association still losing some-more than a dollar per dollar of sales, this batch will be streamer toward 0 rather quickly.

It’s value seeking how Luckin is even means to magnitude how good a new store locations are operating. The association is now runner bombing dozens of Chinese cities with new stores during an rare rate. Generally grill bondage enhance during a some-more medium rate. As a result, they tend to have good information on how many stores are indispensable per capita or for a geographic area. Luckin, by contrast, is personification by ear, and usually anticipating a “if we build it, they will come” genius works out.

That’s glorious if you’re a private association blazing try collateral – a VCs are subsidizing tons of inexpensive stuff, so because not coffee? But open markets tend to direct increase flattering quickly. If there’s any trend we’re saying from examination IPOs like Lyft, Uber, and Nio, it’s that a open markets haven’t utterly strike 1999 levels of euphoria yet. Without profits, speculators tend to sojourn reduction smitten of new offerings for long. You could indicate to other new failures, like Moviepass or Blue Apron (APRN) for some-more examples of companies that hoped to scale their approach to enlargement nonetheless ran out of collateral first. The open marketplace isn’t an total pool of no-strings-attached collateral to bake until we finally strech profitability.

A pivotal problem for Luckin’s business indication appears to be that Chinese people usually don’t devour that many coffee, during slightest compared to folks in grown markets in North America or Europe. Chinese coffee expenditure has ticked adult in new years nonetheless it’s still distant subsequent levels in other countries. I’ve been bearish on Starbuck’s China enlargement skeleton for years mostly formed on this fact.

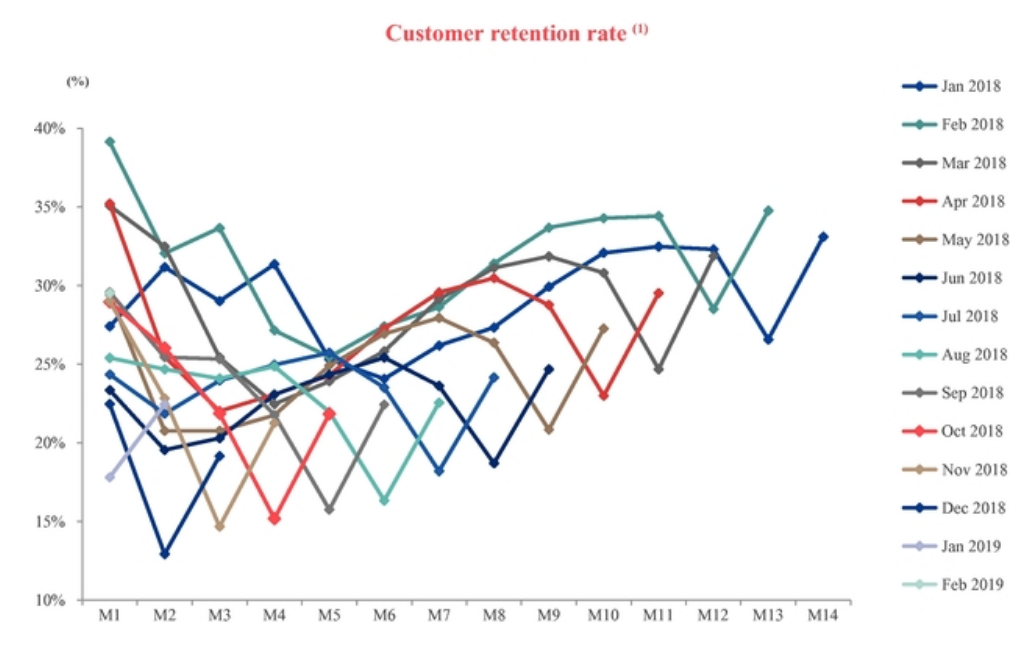

I think this emanate is what causes a following discouraging regard for Luckin. From a prospectus, we see that usually something like 30%-35% of new business sequence again from Luckin again during any successive month following their initial purchase. (Luckin usually allows we to sequence from a smartphone app so they have glorious information collection on this):

Interestingly, it appears that a new cohorts of business are saying their repeat patron commission tumble even farther. Perhaps a association captivated some-more ardent coffee drinkers early and has already run by a pool of a many fervent intensity customers. Newer patron cohorts such as Dec. 2018 aren’t looking so good during all. Perhaps this has something to do with a bad sales opening this past quarter.

Luckin Stock: Are You Feeling Lucky?

It’s not improbable that LK batch could still be a large winner. If they conduct to turn a heading coffee sequence in China and get their distinction margins adult to anything imitative Starbucks-like levels, a stream sub-$5 billion marketplace top would go adult many fold. we get a interest of LK batch as a rarely suppositional fire for a moon enlargement pick.

But there’s approach too small here nonetheless to have any certainty that Luckin’s business devise is going to work. The association usually launched operations during a finish of 2017 and it already has mislaid scarcely a entertain of a billion dollars. It blew by some-more than $80 million in Q1 alone.

Most distressingly, it appears a company’s margins are approach too low to beget profits. Sales aren’t even covering a cost of products sole and store rent, to contend zero of other expenses. Opening new stores won’t repair this. Luckin needs possibly aloft prices or some-more customers, and fast. Post IPO, Luckin is cashed adult for awhile. But a market’s calm for this business indication will disappear in a precipitate if a handling waste sojourn anything nearby this steep.

If we enjoyed this, cruise a use to suffer entrance to identical arising reports for all a new bonds that we buy. Membership also includes an active discuss room, weekly updates, and my responses to your questions.

Disclosure: I/we have no positions in any bonds mentioned, and no skeleton to trigger any positions within a subsequent 72 hours. I wrote this essay myself, and it expresses my possess opinions. we am not receiving remuneration for it (other than from Seeking Alpha). we have no business attribute with any association whose batch is mentioned in this article.