Editor’s note: Seeking Alpha is unapproachable to acquire Value Alpha as a new contributor. It’s easy to turn a Seeking Alpha writer and acquire income for your best investment ideas. Active contributors also get giveaway entrance to SA Pro. Click here to find out some-more »

Investment Thesis

Ten Peaks Coffee (OTC:SWSSF, or TPK on a TSE) is in a primary position to gain on a flourishing approach for specialty and decaf coffee in North America. As we will try to uncover in this article, a association has plain fundamentals, trades during a auspicious gratefulness due to new impact of outmost factors and is proactively operative on augmenting ability in expectation of destiny demand. As an combined kicker, a association offers a ~3.5% division produce during tide prices that appears to be tolerable for a foreseeable future.

Company Overview

TPK is headquartered in Burnaby, British Columbia, Canada, and a primary business is handling a Swiss Water Decaffeinated Coffee Company (SWDCC) that is concerned in a decaffeination routine of immature coffee.

The association reason a rights for a exclusive Swiss H2O decaffeination routine that is a chemical giveaway routine of extracting caffeine from immature coffee beans.

The association has a clever placement channel for a decaffeinated coffee that includes blurb roasters, importers and particular specialty coffee shops.

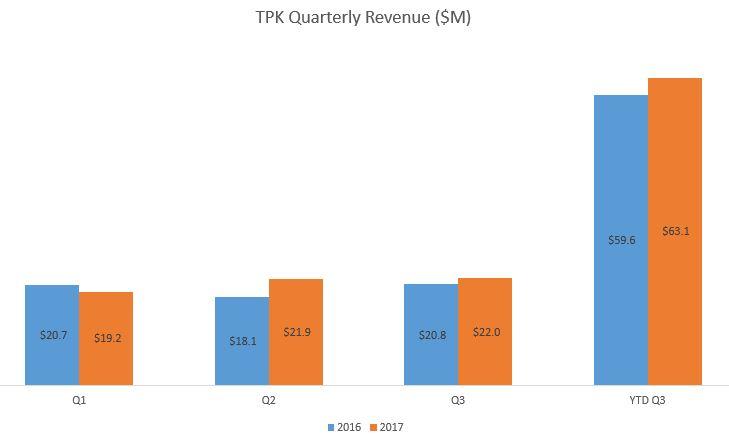

US accounted for ~47% of sum sales for YTD 2017 while Canada was 40%. Remainder was in ubiquitous markets (See Q3 Financials)

Although a association does not directly divulge a customers, my investigate concludes that a company’s business embody Tim Horton’s and Mcdonald’s (Tims decaf coffee has a Swiss H2O routine tag on it (see below) and ex. Tims CEO used to sit on TPK’s board). The association also sells to many (but not all) of a top organic brands sole on Amazon including bulletproof and kicking horse. we have also reached out to many renouned eccentric coffee shops locally that endorse that their decaf coffee is subsequent from a Swiss H2O process. The company’s financier display on their website also lists other logos. (see pg. 4 of financier presentation)

Source: TPK Investor Presentation

TPK generated ~CAD $86M (all dollar sum in this essay in CAD) in income for LTM Q3 2017 during an EBITDA domain of 8.8%. Revenue has grown ~11% CAGR over a past 3 years and a association now has an EV of ~$55M (trading during 7.3x EBITDA). The association also pays a 3.5% division yield. (See Q3 2017 MDA)

The association has really tiny debt on a change piece (24% D/E) and is now in a ~$10M net money position

Industry Overview

Demand for reward peculiarity decaffeinated coffee is rising with a new National Coffee Association consult display that decaf is a fastest flourishing shred of a US coffee market. Total decaffeinated coffee sales are adult year-over-year, with specialty decaffeinated coffee sales being quite strong. The largest consumers of decaf are 18-24 year aged who paint a fastest flourishing shred of a US race and see decaf as a “healthy” option. This shred has also done organic/chemical giveaway a prohibited trend. (See TPK’s 2016 AIF for offer contention on a industry)

The approach for specialty coffee in ubiquitous is also on a arise with many specialty coffee shops popping adult in civic areas and specialty coffee products stuffing adult shelves in a grocery stores and online retailers. This is driven by a augmenting recognition of singular offer coffee pods volume expansion of 12% over 2016. The sum US specialty coffee sales in 2014 were estimated to be $3.5B (see here).

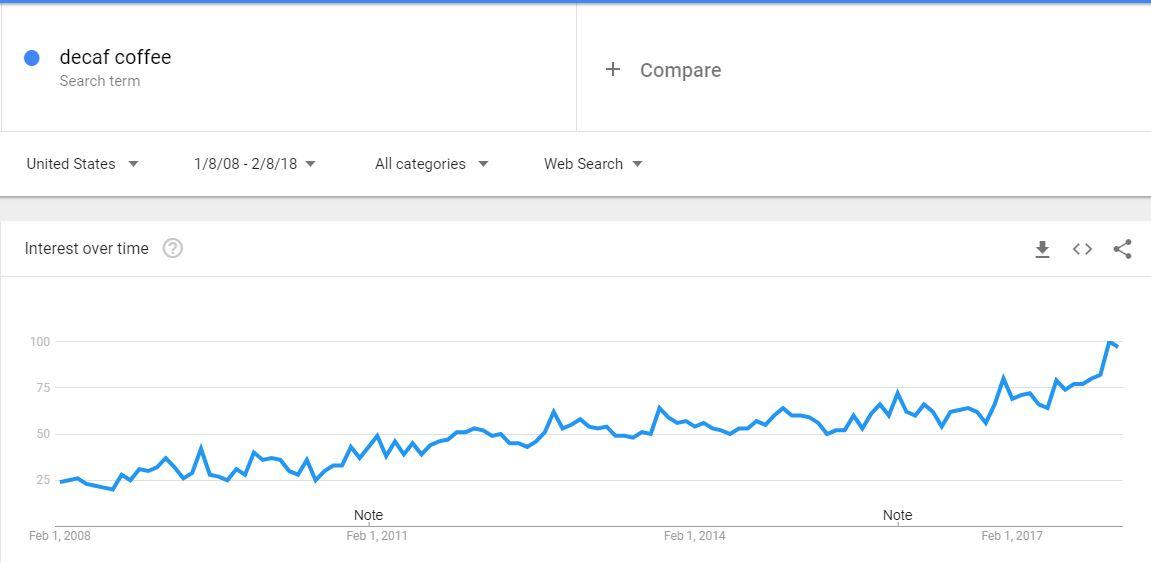

A discerning pointer of a recognition of decaf coffee in a US over a final decade can been seen in a following Google Trends chart:

{kind=link}

Price Decline given Early 2016 and Subsequent Rebound

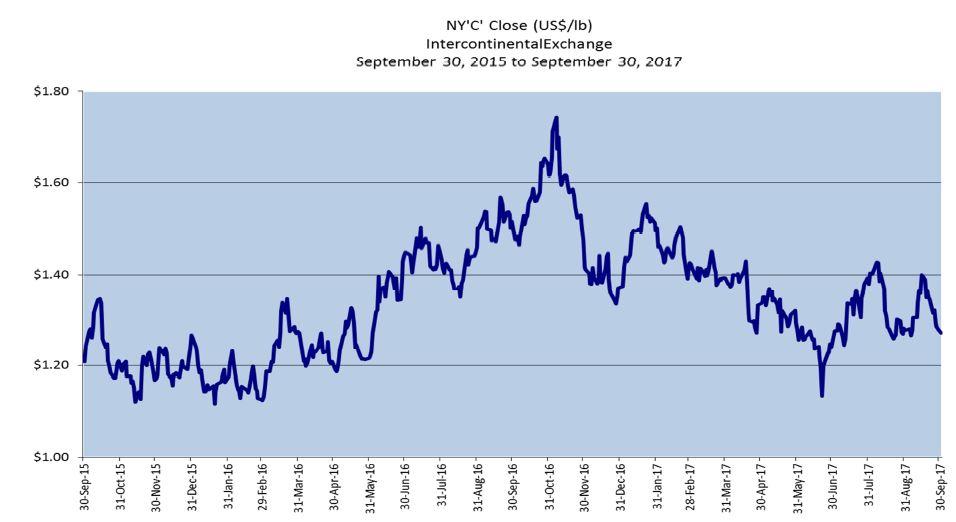

One non-static that plays an vicious purpose in last TPK’s sales volume is a NYC coffee futures cost as a association buys and sells Arabica beans formed on this benchmark. During times of rising futures price, a association will generally knowledge a disappearing volume (albeit aloft offered prices) as importers tend to build inventories when prices are reduce and diminution shopping during aloft cost periods.

The draft next shows a poignant boost in futures prices during 2016 that led to somewhat reduce revenues compared to 2015, however Q4 2016 saw a clever miscarry and sales have been on an ceiling trend given then.

Source: TPK Q3 2017 MDA

{kind=link}

It’s vicious to keep in mind that TPK has a clever hedging module to normalize a impact of sensitivity in coffee futures price. Also, a futures cost is a bigger cause in sales to importers (who sell to other finish users) given TPK’s fastest flourishing sales shred is in specialty coffee accounts that can't means a oppulance of storing vast quantities of coffee and hence are not impacted to a same border by futures prices.

Source: TPK Historical Financial Disclosures

{kind=link}

The batch cost has rebounded given Sep 2017 (~+25%) and in my perspective there is still poignant room to grow.

Growth Catalysts

The association is positioned good to gain on a decaf growth/organic trend from a determined distributor relations and famous code name

TPK has recently stretched ability during a existent plcae and construction of a new estimate plant is underway that is approaching to be operational in 2019. This clearly means that government sees approaching expansion in a business and is holding active stairs to constraint it.

Talking of management, TPK has a rarely regarded comparison government group with estimable knowledge in a industry. As mentioned previously, a ex-Tims CEO used to be on a company’s house that is a vast understanding for such a tiny company.

Given a arise in a specialty coffee industry, a series of incomparable players have recently entered a marketplace that increases a awaiting of TPK being acquired. As an example, Nestle recently acquired a infancy interest in Blue Bottle Coffee for a gratefulness that is believed to be around 5-7x revenue. Blue Bottle is a fast expansion specialty coffee play and a attention could see identical exchange in a future. Interestingly, Blue Bottle patron use reliable that their decaf is subsequent from a Swiss H2O process. TPK could be a good straight formation aim for a vast actor that is already in a specialty coffee market.

Valuation

The batch is now trade during LTM EV/EBITDA of ~7.3x, given historically it has traded around 10-12x. Given destiny expansion prospects, it is not formidable to see a gratefulness mixed returning to a chronological average.

Most approach competitors are not publicly traded therefore a severe to get good comps. Feel giveaway to indicate out suitable comps in a comments so we can labour my analysis.

A singular tender with TPK is a 3.5% division produce that is really singular for a association of this size. The division has been in place for several years (at slightest given 2011) and appears to be tolerable given a company’s expansion prospects and a payout ratio of ~40%.

Key Risk Factors

The association has embarked on a construction of a new trickery that requires estimable collateral ($35M). Although a association appears to have sufficient appropriation to finish this project, there is always a risk of plan delays that can outcome in mislaid income and additional costs.

The association derives ~38% income (2016) from tip 3 customers

Long tenure increases in coffee future’s prices and a diseased USD can drag down revenues. Fx impact is due to infancy of sales being in USD while losses being paid in CAD.

The association has a really tiny marketplace top and we could not find any researcher coverage (which could be a good pointer depending on that approach we see it). The association also has sincerely low trade volumes.

Conclusion

I trust TPK has clever fundamentals, constrained expansion prospects, an appealing division produce and a auspicious gratefulness that aver a deeper demeanour from investors seeking a batch that provides a protected income tide along with cost appreciation potential.

Disclosure: I am/we are prolonged SWSSF.

I wrote this essay myself, and it expresses my possess opinions. we am not receiving remuneration for it (other than from Seeking Alpha). we have no business attribute with any association whose batch is mentioned in this article.